Pressure is mounting for new car prices to be slashed after sales plunged to their lowest for 50 years in January.

Buyers who cannot visit showrooms during lockdown and who are concerned about jobs and income have put the brakes on business and now manufactuers face fines if they cannot reduce their fleet average this autumn.

More sales have moved on-line and the industry and trade expect this to continue even when lockdown ends, possibly before March, but it will come too late to help the traditionally highest selling month when the new 21-number plate is released.

Dealers offering the best prices backed by manufacturer “contributions”, low rate finance and pcp contracts have moved ahead of rivals which are not so generous and the perceived premium brands have seen buyers turning to them for the stronger residual value they traditionally hold.

The UK new car market fell -39.5% in January with 59,030 fewer registrations compared to the same month last year, said the Society of Motor Manufacturers and Traders with 90,249 cars registered as showrooms across the country remained shut, leading to the worst start to the year since 1970.

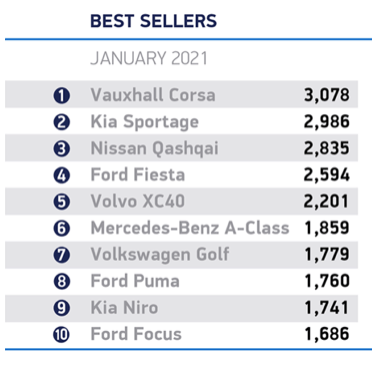

Only Smart and Porsche increased their sales and share while Ford held onto their market lead but are now closely chased by Volkswagen.

Demand remained depressed for both private buyers (-38.5%) and large fleets (-39.7%). Declines were also recorded in both petrol and diesel cars registrations, which fell by -62.1% and -50.6% respectively.

On a positive, however, battery electric vehicle (BEV) uptake grew by 2,206 units (54.4%) to take 6.9% of the market, as the number of available models almost doubled from 22 in January 2019 to 40 this year. Combined, BEVs and plug-in hybrid vehicles (PHEVs) accounted for 13.7% of registrations.

There can be no let-up in the pace of environmental improvement, however, as the industry must achieve a UK-only CO2 fleet average target of 95g/km this year or face severe penalties. This underscores the need to get showrooms open as soon as Britain emerges from lockdown, so they can generate the demand required to reach the country’s green goals.

“As expected new car sales fell -39.5% as a result of the January lockdown, but retailers are optimistic about the year ahead, provided that dealerships will be allowed to reopen as soon as it is safe to do so”, said Sue Robinson, Chief Executive of the National Franchised Dealers Association, which represents franchised car and commercial vehicle retailers.

Sue Robinson added, “Franchised dealers continue to offer ‘click & collect’ and deliveries to customers, and aftersales servicing to keep key workers on the road, however, there is a proportion of consumers waiting for dealerships to reopen and holding off their vehicle purchases due to the current restrictions. Showrooms have spacious areas and dealers can work by appointment ensuring the safety of customers and staff.

“Positively, sales of electrified vehicles have begun the year with a strong performance and with more models coming to the market, the improvement to the charging infrastructure and retailers investing heavily to inform their customers, sales of EVs will continue to grow.

“Despite the lockdown, the automotive retail sector is looking at 2021 with confidence as sales will likely be fuelled by pent-up demand, rising registrations of low and zero emission vehicles and the increasing importance of car ownership, which is seen by more and more people as the safest mean of personal transport in the present climate”.

James Fairclough, CEO of AA Cars, added, “Car dealerships began the new year closed due to the lockdown and unfortunately without any idea of when they may re-open, slowing the number of new car sales to a trickle.

“Nevertheless this lockdown is likely to be different to the shutdown last spring. Many dealers have adapted their proposition, and increasing numbers are now offering home delivery and click and collect options.

“Digitalising elements of the sales process has no doubt been challenging for many, but the industry’s effort and agility will pay off in the long-run – as we expect some drivers will prefer to buy in this way in the future.”

He went on, “In the short-term, the focus is on two crucial questions – when will dealerships be allowed to reopen, and what will be the impact of the new registration plates introduced at the start of March?

“New plates typically give sales a welcome boost, but the benefit could be muted if forecourts remain closed to the public. The fact that lockdown is also making it more difficult for customers to sell their existing cars could potentially dampen demand further.

“The challenge will be for dealers to capitalise on the new plates by using their new lockdown-friendly sales channels. There is light at the end of the tunnel, and the industry will come out of the pandemic stronger, and with a wider variety of purchasing and selling methods available to customers.

Alex Buttle, director of used car marketplace Motorway.co.uk, took the viewpoint of the second-hand market, “Record-setting low new car registrations wasn’t the start we wanted to the year, but focusing on the positives, it’s encouraging to see continued growth of electric car sales as a % of total sales, after 2020 saw the number of EVs surpass diesel vehicles sold for the first time ever.

“The time is now for the Government to accelerate the uptake of EVs and capitalise on a growing consumer appetite for next-generation cars. Overall, the picure is too challenging for the new car industry to boom right now. While the industry was hoping to start the New Year with a bang, that hope evaporated as much of the UK went into lockdown for the third time.”

Experian today launched the newest version of its fraud prevention platform to help businesses dealing with the rapid surge in demand for digital services and the growth of online accounts.

Due to the digital acceleration instigated by Covid-19, online retailers, businesses, and their customers are at risk of the growing threat from fraudsters exploiting outdated and unsophisticated fraud prevention systems.

The size of the problem is significant. Experian estimates that 10 billion identity authentication checks are currently being made each day globally. Up to £31 billion* is set to be lost via online payment fraud in 2024 if rates continue at their current speed.

Specifically, Account Takeover fraud (ATO) – where a fraudster gains unauthorised access to a legitimate customer account – has increased by 34%**. It is likely to become an even bigger issue as people access more services online.

To counter the threat and meet the demands of this new world, Experian has upgraded and enhanced its CrossCore platform. Incorporating the latest machine learning analytics capability, behavioural biometrics and device recognition technology, the single API solution gives businesses a multi-faceted approach to monitoring and reviewing suspicious activity.